Portfolio 1: Basel-Aligned Multi-Stage Credit Risk Modeling Framework: Development and Application (White-Box model)

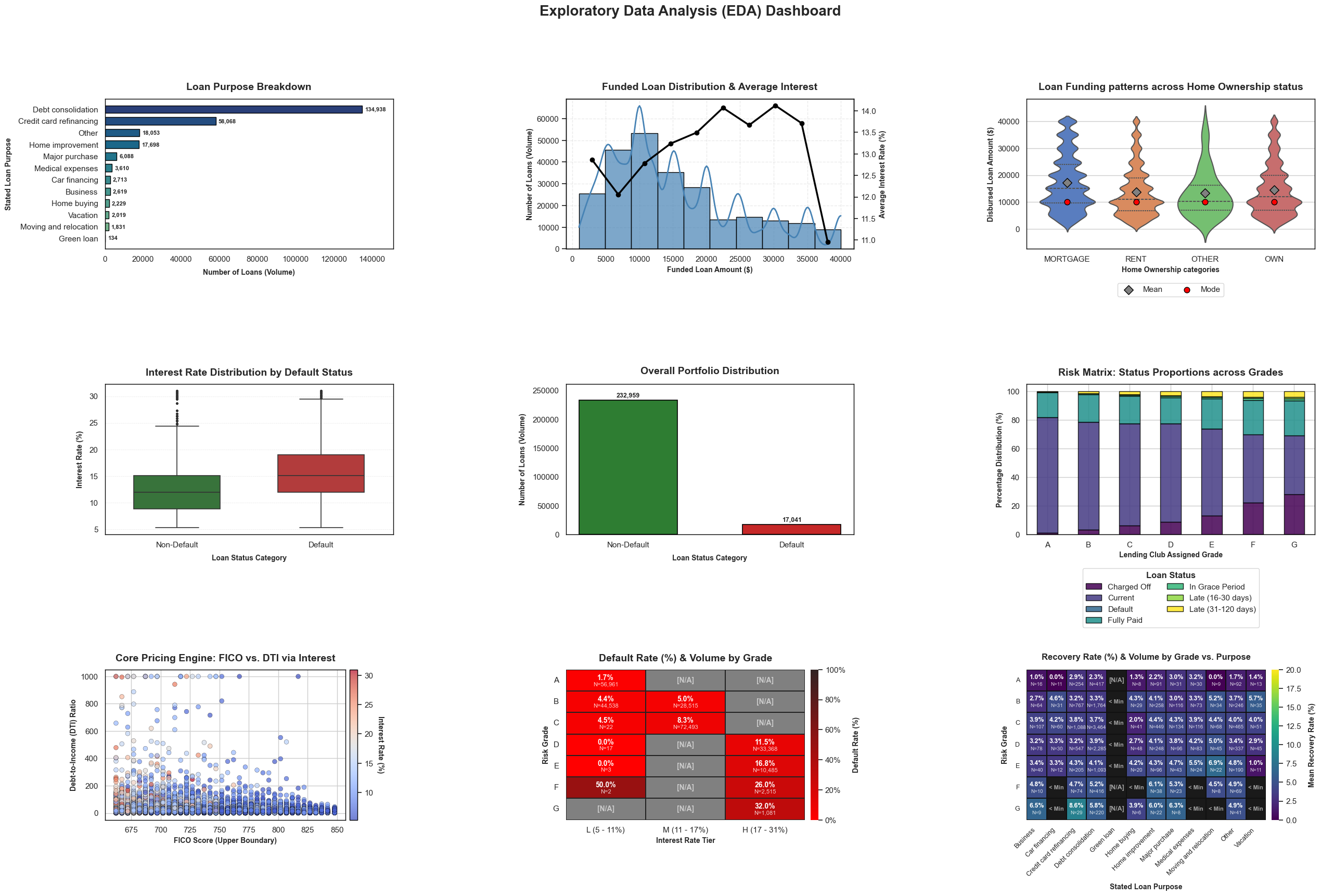

A Basel-aligned multi-stage credit risk modeling framework built on ~250,000 Lending Club consumer loans, estimating Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD) using transparent white-box models. The framework integrates class-weighted logistic regression, a two-stage LGD hurdle model, and Credit Conversion Factor (CCF)-based EAD estimation to generate Expected Loss (EL) forecasts. Independently validated on a 50,000-loan holdout sample, supporting risk-based pricing, stress testing, capital planning, and portfolio credit risk management.

.png)

.png)